Advance Auto Parts

- $993,243

Advance Auto NNN for Sale in Kalkaska, MI — $993K | 7.4% Cap

Kalkaska, Michigan

AutoZone

- $2,005,000

AutoZone NNN for Sale in Homestead, FL — $2.0M | 4.5% Cap

Homestead, Florida

O'Reilly Auto Parts

- $957,188

O’Reilly NNN for Sale in Cabot, AR — $957K | 6.4% Cap

Cabot, Arkansas

Advance Auto Parts

- $1,234,483

Advance Auto NNN for Sale in Mount Orab, OH — $1.2M | 7.25% Cap

Mount Orab, OhioAdvance Auto Parts

- $1,047,273

Advance Auto NNN for Sale in La Grange, KY — $1.0M | 8.25% Cap

La Grange, Kentucky

AutoZone

- $2,975,000

AutoZone NNN for Sale in Rio Grande City, TX — $3.0M | 4.75% Cap

Rio Grande City, Texas

Advance Auto Parts

- $1,600,000

Advance Auto NNN for Sale in Chittenango, NY — $1.6M | 7.5% Cap

Chittenango, New YorkAdvance Auto Parts

- $993,243

Advance Auto NNN for Sale in Kalkaska, MI — $993K | 7.4% Cap

Kalkaska, MichiganAutoZone

- $2,005,000

AutoZone NNN for Sale in Homestead, FL — $2.0M | 4.5% Cap

Homestead, FloridaO'Reilly Auto Parts

- $957,188

O’Reilly NNN for Sale in Cabot, AR — $957K | 6.4% Cap

Cabot, ArkansasAdvance Auto Parts

- $1,234,483

Advance Auto NNN for Sale in Mount Orab, OH — $1.2M | 7.25% Cap

Mount Orab, OhioAdvance Auto Parts

- $1,047,273

Advance Auto NNN for Sale in La Grange, KY — $1.0M | 8.25% Cap

La Grange, KentuckyAutoZone

- $2,975,000

AutoZone NNN for Sale in Rio Grande City, TX — $3.0M | 4.75% Cap

Rio Grande City, TexasAdvance Auto Parts

- $1,600,000

Advance Auto NNN for Sale in Chittenango, NY — $1.6M | 7.5% Cap

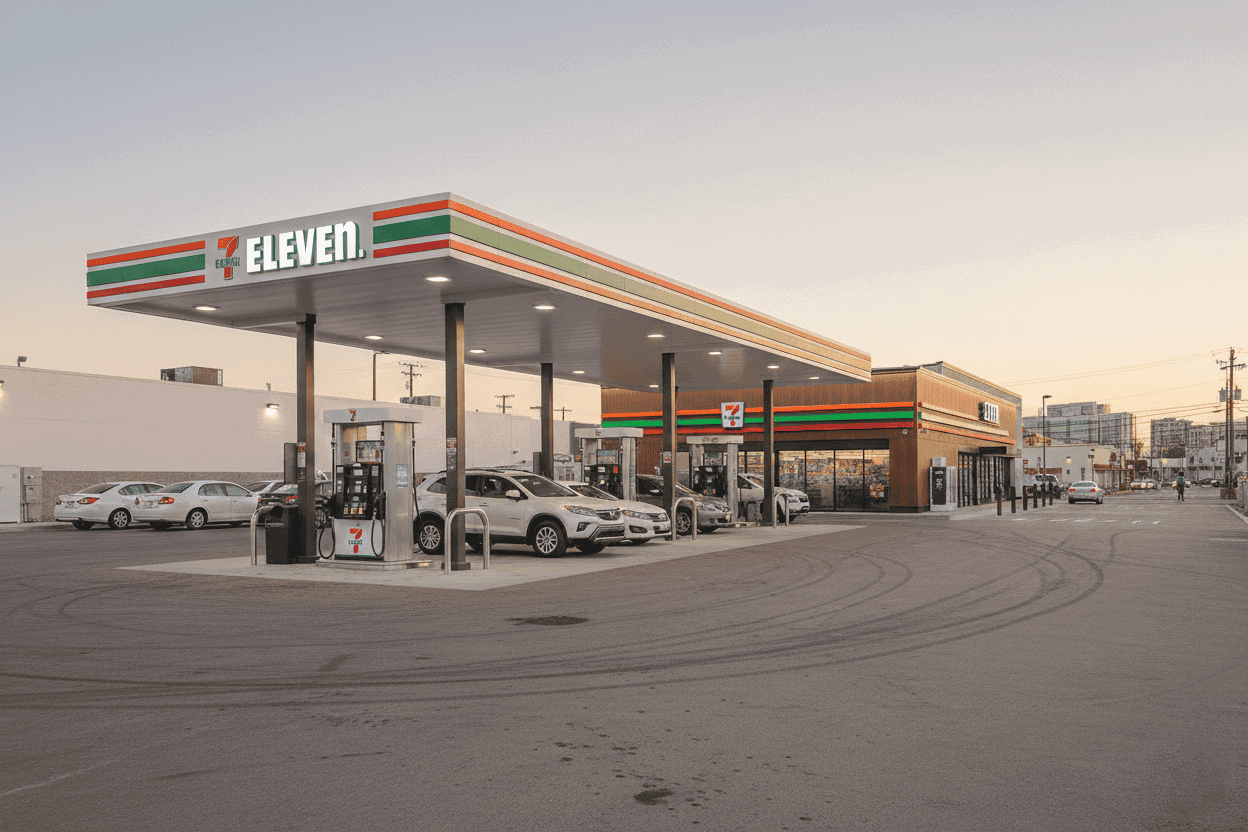

Chittenango, New York7-Eleven NNN Properties for Sale: #1 Convenience Store Investment (2026 Guide)

7-Eleven NNN properties represent America’s leading convenience store chain with 13,000+ US locations and 24/7 operations, which strengthens the long-term reliability of a 7-eleven NNN lease for passive investors.

Investors searching for a 7 eleven for sale will find that 7-Eleven NNN properties represent America’s leading convenience store chain with 13,000+ US locations and 24/7 operations.

providing constant revenue, dual income streams (fuel + merchandise), and investment-grade corporate backing creating exceptional stability for passive income investors seeking high-traffic essential retail.

[afb_listing_carousel

tax_property_type=”automotive”

American Net Lease specializes in 7-Eleven NNN investments nationwide. Browse current listings or call 239.236.2626 to discuss exclusive convenience store opportunities.

Why a 7 Eleven for Sale Is a Strong Investment?

7-Eleven combines the nation’s #1 convenience store footprint (13,000+ US stores, 84,000+ globally) with 24/7 operations ensuring continuous revenue, strategic high-traffic locations, dual profit centers (fuel sales + merchandise), and corporate backing from Seven & i Holdings ($65+ billion Japanese parent), creating unique triple net lease investment opportunities. Investors searching for a 7 eleven for sale should focus on high-traffic locations with corporate guarantees, which maximize both revenue potential and long-term stability.

1. World’s Largest Convenience Store Chain

7-Eleven dominates global convenience retail:

Company overview:

- US stores: 13,000+ locations across America

- Global footprint: 84,000+ stores in 19 countries

- Market position: #1 convenience store globally

- Parent company: Seven & i Holdings (Tokyo: 3382)

- Market cap: $65+ billion (parent company)

- Founded: 1927 (nearly 100 years operating history)

Business model:

- Franchised: 95%+ of US stores (franchisee-operated)

- Corporate: Select company-operated locations

- Licensing: 7-Eleven brand globally recognized

- Support: Corporate provides systems, marketing, supply chain

- Revenue model: Franchise fees + real estate ownership/leasing

Store economics:

- Average size: 2,400-3,200 sq ft (compact footprint)

- Fuel pumps: 8-12 positions typical (4-6 MPDs)

- Inside sales: $1.2M-2M+ annually (varies by location)

- Fuel gallons: 100K-300K+ monthly (high-volume sites)

- Operating hours: 24/7/365 (continuous operations)

#1 convenience brand + Global scale = Strong tenant

2. 24/7 Operations & Continuous Revenue

7-Eleven never closes:

24-hour advantage:

- Open all day, every day (365 days/year)

- No downtime: Revenue generation continuous

- Night shift: 30-40% of sales (late-night consumers)

- Emergency purchases: Customers need 24/7 access

- Competitive edge: Many competitors close overnight

Customer traffic patterns:

- Morning rush: 6-9 AM (coffee, breakfast, commuters)

- Lunch: 11 AM-2 PM (sandwiches, snacks, beverages)

- After work: 4-7 PM (dinner items, beer/wine, gas)

- Late night: 10 PM-2 AM (snacks, drinks, essential items)

- Overnight: 2-6 AM (shift workers, travelers, emergencies)

Revenue implications:

- Sales spread across 24 hours (not just day shift)

- Higher total sales volume (vs limited hours)

- Attracts locations: Hospitals, airports, highways

- Customer loyalty: “Always open when I need it”

Operational stability:

- Labor costs higher (24/7 staffing)

- BUT sales justify (revenue covers expenses)

- Security: LED lighting, cameras (crime deterrent)

- Franchise support: 24-hour corporate assistance

24/7 = Maximum revenue generation + Essential service positioning

3. Dual Revenue Streams: Fuel + Merchandise

7-Eleven captures customers twice:

Fuel revenue (high volume, low margin):

- Fuel sales: 60-70% of total revenue

- Margin: 10-20 cents per gallon typical

- Volume: 100K-300K gallons monthly

- Fuel profit: $10K-60K monthly (varies by volume/margin)

- Traffic driver: Customers come for gas, buy inside

Merchandise revenue (lower volume, high margin):

- Inside sales: 30-40% of total revenue

- Margin: 30-40% gross profit typical

- Categories: Beverages, snacks, food, tobacco, lottery

- Merchandise profit: Often exceeds fuel profit

- Higher margin = More profitable per dollar sold

Synergy between fuel and merchandise:

- Fuel brings traffic (customers filling up)

- 60-70% buy something inside (impulse purchases)

- Merchandise margin offsets fuel competition

- Combo = Resilient business model

Proprietary products:

- Slurpee: Iconic frozen beverage (high margin)

- Big Gulp: Large fountain drinks (brand recognition)

- Hot foods: Pizza, sandwiches, breakfast (food service)

- Private label: 7-Select brand (exclusive products)

Dual streams = Diversified revenue, recession resilience

4. Strategic High-Traffic Locations

7-Eleven targets maximum visibility:

Location strategy:

- Corner lots: Signalized intersections preferred

- Highway exits: Interstate visibility, traveler traffic

- Urban density: Metropolitan areas, dense suburbs

- Commuter corridors: Daily traffic patterns

- Residential proximity: Walk-in customer base

Traffic requirements:

- Vehicle count: 15,000-30,000+ daily (minimum)

- Urban: Higher foot traffic, less fuel focus

- Suburban: Balanced fuel + merchandise

- Highway: Fuel-dominant, traveler focus

Competitive positioning:

- First-mover advantage: Secures best corners early

- Site selection: Sophisticated analytics

- Real estate control: 7-Eleven often owns land

- Long-term hold: Not relocating frequently

Demographics targeted:

- Middle income: $40K-$80K household income

- Age: 18-54 (broad appeal)

- Daily commuters: Regular repeat customers

- Families: Convenience for busy households

High traffic = High sales volume + Property value stability

5. Investment-Grade Corporate Backing

Seven & i Holdings provides institutional strength:

Parent company (Seven & i Holdings):

- Tokyo Stock Exchange: 3382

- Market cap: $65+ billion (JPY 10+ trillion)

- Revenue: $80+ billion annually

- Operating income: $3+ billion

- Credit rating: BBB- investment grade (S&P)

Diversified portfolio:

- 7-Eleven: Global convenience leader

- Speedway: Acquired 2021 ($21B, 3,900+ stores merged into 7-Eleven)

- Ito-Yokado: Japanese supermarkets

- Department stores: Sogo & Seibu (Japan)

- Financial services: 7-Bank in Japan

US operations:

- 7-Eleven Inc: US subsidiary

- Headquarters: Irving, Texas

- Corporate guarantee: Varies by deal structure

- Franchise model: Most stores franchisee-operated

- Real estate: Corporate owns/leases, then sublet to franchisees

Financial strength:

- Consistent profitability: 97 years operating history

- Global diversification: Revenue across 19 countries

- Speedway acquisition: $21B investment = commitment to US market

- Cash generation: Strong free cash flow

Corporate backing = Stability + Long-term commitment

6. Franchise Model & Lease Structure

Understanding 7-Eleven NNN lease complexity:

Corporate vs franchisee:

- Corporate-operated: 7-Eleven Inc operates directly

- Franchised: Local operator under 7-Eleven license

- Corporate guarantee: Required for NNN investor protection

- Lease structure: Corporate master lease, franchisee sublease

Typical lease terms:

- Initial term: 15-20 years (corporate guarantee)

- Renewal options: 2-4 five-year periods

- Rent increases: 10% every 5 years or 1.5-2% annually

- Triple net: Tenant pays property tax, insurance, maintenance

- Guarantor: 7-Eleven Inc (not franchisee individual)

Critical lease provisions:

- Corporate guarantee: Essential (verify Seven & i or 7-Eleven Inc)

- Performance clauses: Rare but review (sales thresholds)

- Relocation rights: Sometimes included (franchisee may move)

- Fuel tank compliance: Environmental responsibility (review)

- Renewal likelihood: Strong locations 70-80%

Speedway integration:

- 3,900+ Speedway stores acquired 2021

- Converting to 7-Eleven brand (multi-year process)

- Real estate implications: Some closures/consolidations

- Due diligence: Verify if former Speedway (integration status)

Lease structure critical = Verify corporate guarantee specifics

7. Reasonable Cap Rates for C-Store Sector

7-Eleven properties balance location quality with yields:

Typical cap rates by location (2026):

- Highway/Interstate: 6.5-7.5% (highest volume, fuel-focused)

- Suburban high-traffic: 6.0-7.0% (balanced fuel + merchandise)

- Urban dense areas: 5.5-6.5% (lower fuel, high inside sales)

- Secondary markets: 7.0-7.5% (established but lower traffic)

Cap rate drivers:

- Credit quality: BBB- investment grade (moderate caps)

- Location: Highway premium, urban stability

- Fuel volume: Higher gallons = lower caps (more valuable)

- Lease term: 15-20 years = stability

- Store format: Newer larger stores = premium

Price range:

- Highway high-volume: $3M-6M+

- Suburban established: $2M-3.5M

- Urban dense: $2.5M-4M

- Secondary markets: $1.5M-2.5M

Returns analysis:

- Cap rate: 6-7.5% income

- Appreciation: 2-4% (location-dependent)

- Total return: 8-11.5% potential

- Fuel volatility: Margins fluctuate (merchandise stabilizes)

C-store sector = Higher yields than QSR, lower than dollar stores

8. Essential Service & Recession Resilience

7-Eleven thrives in all economic environments:

Essential service factors:

- Fuel: Non-discretionary (people need to drive)

- Convenience: Time-saving (value in busy lives)

- Food/beverages: Daily necessities (coffee, milk, bread)

- Tobacco/lottery: Habitual purchases (recession-resistant)

- Emergency items: Late-night needs (always required)

Recession performance (2008-2009):

- Store traffic: Maintained (essential purchases)

- Fuel sales: Slight decline (less driving) but stabilized

- Inside sales: Resilient (value focus, smaller purchases)

- Store closures: Minimal (strong locations survived)

- Market share: Gained (independent operators closed)

COVID-19 pandemic (2020-2021):

- Essential business: Stores remained open

- Fuel sales: Declined initially (lockdowns) then recovered

- Merchandise: Strong (convenience valued, stockpiling)

- Expansion: Speedway acquisition during pandemic ($21B)

- Resilience: Demonstrated essential service positioning

Value proposition during downturns:

- Cheaper than restaurants: Prepared food value

- Closer than supermarkets: Convenience saves time/gas

- Small purchases: $5-20 transactions manageable

- Immediate gratification: No delivery wait

Essential + Convenient = Recession-resistant tenant

7-Eleven NNN Investment Strategies

Highway Interstate Exits

Maximum fuel volume locations:

Target characteristics:

- Interstate highway exits (I-5, I-95, I-10, etc.)

- Truck traffic: Commercial drivers frequent customers

- Traveler traffic: Road trip fill-ups, snacks

- Fuel volume: 150K-300K+ gallons monthly

- Visibility: Highway signage, easy on/off access

Advantages:

- Highest fuel sales (volume drives revenue)

- Strong merchandise (travelers buy snacks/drinks)

- Consistent traffic (highways don’t close)

- Less local competition (interstate advantage)

- Appreciation: Highway properties stable value

Investment profile:

- Purchase: $3M-6M+

- Cap rate: 6.5-7.5%

- Lease: 15-20 years

- Focus: Fuel volume + High yields

Considerations:

- Fuel price sensitivity (margin compression risk)

- Environmental compliance (underground tanks)

- Economic cycles (less driving = volume drop)

Fuel-volume focused investors

Urban Dense Metropolitan

High merchandise sales locations:

Target characteristics:

- Dense urban neighborhoods (NYC, SF, Chicago, Boston)

- Walk-in traffic: Residential density, foot traffic

- Transit proximity: Subway, bus stops nearby

- Inside sales focus: Less fuel, more merchandise

- 24/7 advantage: Night shift workers, late-night customers

Advantages:

- Property appreciation: Urban real estate growth

- Merchandise margin: Higher-profit products

- Stable traffic: Dense population base

- Less fuel dependency: Inside sales primary

- Recession resilience: Urban density maintains traffic

Investment profile:

- Purchase: $2.5M-4M

- Cap rate: 5.5-6.5%

- Lease: 15-20 years

- Focus: Urban appreciation + Merchandise

Considerations:

- Lower yields (urban premium pricing)

- Smaller footprint (space constraints)

- Parking limitations (urban density)

Appreciation-focused urban investors

Suburban Commuter Corridors

Balanced fuel + merchandise:

Target characteristics:

- Major suburban arterials (traffic 20K-30K daily)

- Commuter corridors: Daily predictable traffic

- Residential proximity: Neighborhood access

- Balanced sales: 60% fuel, 40% merchandise

- Corner location: Signalized intersection

Advantages:

- Balanced revenue: Both streams healthy

- Predictable traffic: Daily commuter patterns

- Demographics: Middle/upper-middle income

- Stability: Suburban growth markets

- Yields: 6-7% reasonable

Investment profile:

- Purchase: $2M-3.5M

- Cap rate: 6.0-7.0%

- Lease: 15-20 years

- Focus: Balance + Stability

Balanced income + growth investors

Secondary Market Established

Proven performers in smaller metros:

Target characteristics:

- Regional cities: 100K-500K population

- Established location: 10+ years operating

- Local dominance: Limited competition

- Demographics: Working/middle class

- Fuel + merchandise: Both revenue streams

Advantages:

- Higher yields: 7-7.5% caps

- Lower entry: $1.5M-2.5M

- Proven history: Operating track record

- Less competition: Fewer institutional buyers

- Stable market: Established customer base

Investment profile:

- Purchase: $1.5M-2.5M

- Cap rate: 7.0-7.5%

- Lease: 10-20 years

- Focus: Yield + Cash flow

Income-focused investors seeking higher returns

Evaluating 7 Eleven for Sale Locations for Maximum ROI

Critical Location Analysis

7-Eleven performance is location-dependent:

Traffic & visibility:

- Vehicle count: 15,000-30,000+ daily minimum

- Corner location: Signalized intersection ideal

- Highway access: Interstate exits premium

- Visibility: Signage visible from road

- Ingress/egress: Easy in-and-out access

Demographics:

- Population: 10,000+ within 3-mile radius

- Median income: $40K-$80K household

- Age: 25-54 primary (working population)

- Commuters: Daily predictable traffic

- Employment: Job centers nearby

Competition assessment:

- Other 7-Eleven: Within 2-3 miles (saturation?)

- Circle K, Wawa, Sheetz: Direct c-store competition

- Gas stations: Shell, BP, Chevron with c-stores

- Dollar stores: Alternative for snacks/beverages

- Market share: 7-Eleven dominance or fragmented

Fuel dynamics:

- Fuel pumps: 8-12 positions (4-6 MPDs) ideal

- Gallons monthly: 100K-300K+ (verify volume)

- Pricing: Competitive with nearby stations

- Margin: 10-20 cents per gallon typical

- Fuel supplier: Contract terms (review)

Store Performance Evaluation

Critical 7-Eleven metrics:

Sales indicators (if available):

- Strong: $2M-4M+ total annual sales

- Fuel: 100K-300K gallons monthly (volume)

- Inside: $1.2M-2M+ merchandise annually

- Average: $1.5M-2.5M total sales

- Weak: Under $1.5M (investigate)

Operating characteristics:

- Format: Standard 2,400-3,200 sq ft

- Fuel: Multi-product dispenser (MPD) positions

- 24/7: Confirmed (some rural may close overnight)

- Proprietary: Slurpee, Big Gulp, hot food present

- Technology: Payment systems, loyalty app integration

Speedway conversion status:

- Former Speedway: Acquired 2021 (3,900+ stores)

- Conversion timeline: Multi-year to 7-Eleven brand

- Integration: Some closures/consolidations occurring

- Due diligence: Verify conversion status, lease terms

Red flags:

- Declining sales: Multiple years downward trend

- Speedway overlap: Multiple stores close together

- Fuel tank issues: Environmental compliance problems

- Franchise turnover: Multiple operators in short time

- Deferred maintenance: Aging equipment, building condition

Lease Structure Review

Critical 7-Eleven lease provisions:

Guarantor verification (CRITICAL):

- 7-Eleven Inc: Required (US subsidiary)

- Seven & i Holdings: Acceptable (parent company)

- Franchisee only: NOT ACCEPTABLE (need corporate)

- Credit rating: BBB- confirmed (investment grade)

- Guarantee term: Full initial lease term minimum

Lease length:

- 15-20 years: Preferred (stability)

- 10-15 years: Acceptable (verify renewals)

- Under 10 years: Higher risk (re-leasing soon)

Rent structure:

- Base rent: Fixed monthly amount

- Escalations: 10% every 5 years or 1.5-2% annually

- Percentage rent: Sometimes (rare in NNN)

- Options: 2-4 five-year renewals typical

Special provisions:

- Environmental: Fuel tank responsibility (CRITICAL)

- Above-ground tanks: Lower risk

- Underground: Verify compliance, insurance

- Liability: Tenant vs landlord (negotiate)

- Relocation: Franchisee may move (review carefully)

- Performance: Sales thresholds (rare but scrutinize)

- Renewal: Automatic or at tenant option

Environmental due diligence (ESSENTIAL):

- Phase I ESA: Required (environmental assessment)

- UST compliance: Underground storage tank testing

- LUST: Check for leaking underground storage tanks

- Remediation: Past contamination cleaned up?

- Insurance: Environmental liability coverage

Financial Underwriting

7-Eleven property analysis:

Revenue verification:

- Rent: Verify current base rent amount

- Escalations: Calculate future rent increases

- Renewal options: Project renewal rent

- CAM/NNN: Verify tenant pays (triple net)

Expense estimation:

- Property tax: 1-2% of property value annually

- Insurance: $2,000-$5,000+ (fuel increased premium)

- Maintenance: Minimal (tenant responsibility)

- Management: 3-5% if using property manager

- Reserves: 3-5% for major repairs

Cap rate analysis:

- Market cap rate: 6-7.5% typical range

- Your cap rate: Calculate (NOI / Purchase Price)

- Compare: Similar 7-Eleven sales in area

- Risk adjustment: Location quality, lease term

Cash flow projection:

- Year 1-5: Base rent

- Year 6-10: After first escalation (+10%)

- Year 11-15: After second escalation (+10%)

- Year 16-20: After third escalation (+10%)

- Renewal: Conservative assumption (70-80% likelihood)

Current 7-Eleven NNN Properties for Sale

Featured 7-Eleven NNN Listings:

Looking for specific 7-Eleven properties by market? Contact our specialists at 239.236.2626 for exclusive nationwide opportunities.

7-Eleven Investment Case Study

Investment Profile: 7-Eleven – Dallas Suburban Highway Exit

Property Details:

- Tenant: 7-Eleven Inc (subsidiary of Seven & i Holdings)

- Guarantee: Corporate guarantee (BBB- credit rating)

- Purchase Price: $3,200,000

- Cap Rate: 7.0%

- Annual NOI: $224,000

- Lease Term: 18 years (franchisee-operated, corporate lease)

- Rent Increases: 10% every 5 years

- Location: Plano, Texas (Dallas northern suburb)

Property Features:

- Highway access: I-75 (Central Expressway) exit

- 2,800 sq ft convenience store

- 10 fuel pumps (5 MPDs), high-volume location

- Corner lot, 0.6 acres

- Traffic count: 28,000 vehicles/day

- Build date: 2018 (newer format)

Market Details:

- Plano: Median income $95,000 (affluent suburb)

- Population: 50,000+ within 3-mile radius

- Employment: Corporate headquarters nearby (Toyota, Liberty Mutual, JPMorgan Chase)

- Commuter corridor: Daily predictable traffic

- Competition: Limited (nearest c-store 1.5 miles)

Sales performance:

- Fuel: 180,000 gallons monthly (high volume)

- Inside: $1.8M annually (strong merchandise)

- Total: $3.5M+ annual sales (excellent performance)

- Franchisee: Established operator, 5 locations in Dallas

Investor Profile: California 1031 exchange investor. Sold Bay Area apartment building ($4.5M, $2M gain). Sought: exit California 13.3% tax, Texas 0% tax advantage, convenience store exposure, higher cap rate, corporate guarantee stability.

Tax advantage:

- Annual NOI: $224,000

- California state tax saved: $29,912 (13.3%)

- Texas state tax: $0 (0%)

- Annual tax savings: $29,912 (CA vs TX)

- 18-year tax savings: $538,416

Performance to date:

- Purchase: June 2023

- Current: February 2026 (32 months)

- 100% on-time rent payments

- Franchisee performance: Strong (sales growing)

- Property value: Estimated $3,520,000 (10% appreciation)

- Plano market: Continued corporate growth

18-Year Income Projection:

- Years 1-5: $224,000 annual NOI ($1.12M cumulative)

- Years 6-10: $246,400 annual NOI (+10%, $1.232M cumulative)

- Years 11-15: $271,040 annual NOI (+10%, $1.355M cumulative)

- Years 16-18: $298,144 annual NOI (+10%, $894,432 for 3 years)

- Total 18-year income: $4,601,432

- CA tax savings: $538,416 (vs California ownership)

- Projected value (Year 18): $4M+ (Plano appreciation)

- Total return: 120%+ over 18 years (income + appreciation + tax)

Investor testimonial: “This 7-Eleven in Plano is exactly what I wanted. I’m getting 7% cap rate vs 4-5% I’d get on apartments in the Bay Area, and I’m saving $30,000 a year in California state taxes since Texas has zero income tax. The location is bulletproof—right off I-75 with 28,000 cars a day, affluent demographics, and corporate headquarters all around. The franchisee is crushing it with 180,000 gallons of fuel monthly and nearly $2M in inside sales. Corporate guarantee from 7-Eleven gives me confidence even though it’s a franchisee operating it.”

Frequently Asked Questions

Are 7-Eleven NNN properties safe investments?

Yes, 7-Eleven NNN properties are generally safe when properly underwritten.

Strengths: BBB- investment-grade credit (Seven & i Holdings $65B+ parent), #1 convenience store (13,000+ US stores, 84,000+ globally), 24/7 operations (continuous revenue), dual revenue (fuel + merchandise diversification), essential service (recession-resistant).

Risks: Franchise model (verify corporate guarantee), environmental liability (fuel tanks), fuel margin volatility (margins fluctuate with oil prices), Speedway integration (3,900 stores acquired, some consolidation).

Safety factors: Require 7-Eleven Inc or Seven & i corporate guarantee (NOT franchisee only), conduct Phase I Environmental Site Assessment (fuel tanks), verify high traffic (20,000+ vehicles daily), confirm strong sales ($2M+ annually if data available).

High-volume locations with corporate guarantee and clean environmental history are very safe; marginal locations with weak guarantees carry real risk.

What are typical cap rates for 7-Eleven properties?

7-Eleven NNN properties offer 6-7.5% cap rates depending on location and fuel volume.

Highway/Interstate exits: 6.5-7.5% (highest volume, fuel-dominant), Suburban high-traffic: 6-7% (balanced fuel + merchandise), Urban dense: 5.5-6.5% (lower fuel, strong inside sales), Secondary markets: 7-7.5% (established, lower traffic).

Cap rate drivers: Credit quality (BBB- investment grade), Fuel volume (higher gallons = more valuable), Location (highway premium, urban stability), Lease term (15-20 years), Store condition (newer larger formats preferred).

Comparison: Higher than QSR (McDonald’s 5-5.5%), Lower than dollar stores (7-7.5%), Similar to gas stations (6.5-7.5%). C-store sector: Higher yields reflect fuel volatility risk, dual revenue provides stability. Focus: Total return = cap rate + appreciation + fuel volume growth potential.

How does 7-Eleven compare to other C-store chains?

7-Eleven NNN properties offer 6-7.5% cap rates depending on location and fuel volume. Highway/Interstate exits: 6.5-7.5% (highest volume, fuel-dominant), Suburban high-traffic: 6-7% (balanced fuel + merchandise), Urban dense: 5.5-6.5% (lower fuel, strong inside sales), Secondary markets: 7-7.5% (established, lower traffic).

A typical 7 eleven for sale offers dual revenue streams from fuel and merchandise, making these locations attractive to investors seeking stable returns.

Cap rate drivers: Credit quality (BBB- investment grade), Fuel volume (higher gallons = more valuable), Location (highway premium, urban stability), Lease term (15-20 years), Store condition (newer larger formats preferred).

Comparison: Higher than QSR (McDonald’s 5-5.5%), Lower than dollar stores (7-7.5%), Similar to gas stations (6.5-7.5%). C-store sector: Higher yields reflect fuel volatility risk, dual revenue provides stability. Focus: Total return = cap rate + appreciation + fuel volume growth potential.

Should I worry about environmental issues with fuel tanks?

Yes, environmental due diligence is CRITICAL for any fuel-related property.

Fuel tank risks: Underground Storage Tanks (USTs) can leak, contaminate soil/groundwater, cost $100K-$1M+ to remediate, create long-term liability.

Essential protections: Phase I Environmental Site Assessment (required, $2K-5K), UST compliance testing (verify tanks meet regulations), Leaking UST (LUST) database check (past contamination?), Environmental insurance (pollution liability coverage), Lease review (tenant vs landlord environmental responsibility).

Who pays for cleanup: Typical NNN lease: Tenant responsible during tenancy, Landlord: Responsible for pre-existing contamination.

Historical: Previous owners may have liability.

Risk mitigation: Buy properties with above-ground fuel tanks (lower risk), Verify UST compliance certification (testing current), Confirm environmental insurance (tenant coverage), Negotiate indemnification (tenant protects landlord), Consider environmental reserve (escrow for potential issues).

Deal-breakers: Known contamination not remediated, Aging USTs (20-30+ years old, high risk), No environmental insurance, Tenant refuses environmental responsibility.

Recommendation: ALWAYS conduct Phase I ESA before purchasing any fuel-related property. Environmental liability can exceed property value—protect yourself.

Can I use 1031 exchange to buy 7-Eleven property?

Yes! 7-Eleven NNN properties are excellent 1031 exchange targets for c-store exposure.

Benefits: Defer capital gains, exit high-tax states (CA 13.3% → TX/FL 0%), essential service exposure (recession-resistant), 24/7 operations (continuous income), corporate guarantee protection.

Popular exchanges: Gas station → 7-Eleven (stay in fuel retail, upgrade to corporate), Apartment → 7-Eleven (simplify to single tenant, reduce management), California property → Texas 7-Eleven (eliminate state tax, maintain cashflow), Retail center → 7-Eleven (consolidate to single property).

7-Eleven 1031 advantages: Wide price range ($1.5M-6M+ accommodates various exchanges), Available nationwide (multiple markets), Corporate guarantee (investment-grade protection), Essential service (long-term stability).

Process: Identify within 45 days, close within 180 days, equal-or-greater value, qualified intermediary. Critical: Verify corporate guarantee (7-Eleven Inc), complete Phase I ESA (environmental), confirm high traffic/sales. We coordinate 7-Eleven 1031 exchanges with full environmental due diligence.

What’s the Speedway acquisition impact on investors?

Seven & i’s $21 billion Speedway acquisition (2021) signals massive US commitment but requires due diligence.

The facts: 3,900 Speedway stores acquired from Marathon Petroleum, Converting to 7-Eleven brand (multi-year process), Some overlap/consolidation occurring (markets with both brands),

Integration: Rebranding, systems, loyalty programs. Investor implications: Positive: $21B investment = long-term US commitment, Scale increases (13,000 → 17,000 stores when complete), Market consolidation (reducing competition).

Concerns: Store closures (overlapping markets being rationalized), Lease changes (some Speedway leases being renegotiated), Brand transition (Speedway loyal customers adjusting).

Due diligence for former Speedway properties: Verify conversion timeline (7-Eleven brand complete?), Check overlap (other 7-Eleven/Speedway nearby = closure risk?), Review lease (guaranteed through conversion?), Confirm sales (performance during transition?).

Protection: Buy 7-Eleven-branded stores (not Speedway), Avoid markets with heavy overlap (3+ stores within 3 miles), Verify corporate guarantee unchanged. Overall: Acquisition strengthens 7-Eleven long-term, but creates short-term consolidation risk in some markets.

Do 7-Eleven stores close frequently?

7-Eleven store closure rate is low for strong locations but rising due to Speedway integration.

Closure factors: Store performance (weak sales = closure risk), Speedway overlap (duplicate markets being consolidated), Franchise turnover (operator exits, store may close temporarily), Real estate issues (lease expiration, relocation), Competition (new c-stores nearby).

Historical closure rate: Strong locations: 5-10% over 20 years (very stable), Weak locations: 20-30% over 20 years (higher risk), Speedway impact: Temporary increase (integration closures).

Protection strategies: Buy high-volume locations (180K+ gallons fuel, $1.5M+ inside sales), Avoid Speedway overlap markets, Verify long-term lease (15-20 years = commitment signal), Strong demographics (20,000+ daily traffic, affluent income), Corporate guarantee (ensures rent even if closed).

Renewal likelihood: Strong performers: 75-85% renewal rate, Average performers: 60-75%, Weak performers: 40-60% (may not renew).

Red flags indicating closure risk: Declining sales (multiple years downward), Speedway nearby converting to 7-Eleven, Franchise operator turnover (multiple in short time), Deferred maintenance (corporate not investing).

Due diligence critical: Request sales data, verify traffic counts, assess competition, confirm corporate commitment.

Is fuel price volatility a concern for 7-Eleven investments?

Yes, fuel margin volatility affects profitability but merchandise diversifies risk. Fuel dynamics: Retail price: Driven by wholesale cost + margin, Margin: 10-20 cents per gallon typical, Volatility: Margins compress when oil prices spike suddenly, Volume: More gallons sold = more total profit despite margin.

Investor protection through diversification: Merchandise sales: 30-40% of revenue, higher margin (30-40% gross profit), Inside sales: More profitable per dollar than fuel, Proprietary products: Slurpee, Big Gulp drive higher margin, Food service: Hot food, sandwiches add profit.

Why diversification matters: Fuel margin compression: Inside sales offset, Economic cycles: Consumers need convenience items, Recurring customers: Daily traffic less price-sensitive. Historical resilience: 2008 oil spike: Fuel margins compressed but merchandise steady, COVID-19: Fuel dropped initially but inside sales strong, 2022-2023 inflation: Higher prices, stable margins overall.

Landlord perspective (NNN investor): Rent is fixed: Fuel volatility doesn’t change rent payment, Corporate guarantee: 7-Eleven pays regardless of margins, Long lease: 15-20 years provides stability, Dual revenue: Balances overall tenant health. Conclusion: Fuel volatility is real but NNN investors protected by corporate lease + diversified merchandise revenue. Focus on total store performance, not just fuel.

Next Steps: Invest in 7-Eleven NNN Properties

Ready to add America’s #1 convenience store with 24/7 operations to your investment portfolio? American Net Lease provides access to 7-Eleven NNN opportunities nationwide with full environmental due diligence and corporate guarantee verification.

Work With American Net Lease

Why investors choose us for 7-Eleven NNN acquisitions:

- C-store expertise: Fuel volume analysis, environmental due diligence

- Lease verification: Corporate guarantee confirmation (7-Eleven Inc)

- Traffic analysis: Vehicle counts, demographic verification

- Environmental specialists: Phase I ESA coordination, UST compliance

- 1031 exchange coordination: Convenience store portfolio positioning

Schedule Your Free Consultation

Ready to invest in a 7 eleven for sale? Contact our specialists today to explore exclusive NNN opportunities nationwide.

📞 Call: 239.236.2626

📧 Email: Contact Us

🔍 Browse: View All 7-Eleven Properties

Additional Resources

Learn More About C-Store NNN Investing:

- Ultimate Triple Net Lease Guide — Comprehensive NNN education

- Gas Station NNN Properties — Compare fuel-based retail

Compare Investment Markets:

- Florida NNN Properties — Zero-tax opportunity

- Texas NNN Properties — Value leader, zero tax

- Arizona NNN Properties — Growth markets

Explore Other Tenant Types:

- McDonald’s NNN Properties — QSR leader

- Dollar General NNN Properties — Value retail

- Walgreens NNN Properties — Pharmacy leader

Build wealth with 7-Eleven NNN properties—#1 convenience store, 24/7 operations, dual revenue streams. Call 239.236.2626 or request information today.

Last Updated: February 2026